Why should hospitals, pharmacies and pharmacy benefit managers worry about fraud?

Why is pharmacy fraud so important to control?

What should pharmacies do to prevent fraud?

What should those managing prescription drugs expect in cost increases in 2016?

What is so special about COPs?

Ten Questions Hospitals Should Ask Before Embarking on an In-House Pharmacy for Employees

Question One: Can the current in-patient pharmacy fit the needs of employees and dependents?

Question Two: How can the hospital optimize its wholesaler relationship?

Question Three: How can the hospital pharmacy work with the PBM to get into the PBM’s network and at what reimbursement rate?

Question Four: Will bringing the pharmacy cost in-house work with all PBMs?

Question Five: Should plan design differ between the in-house pharmacies and the rest of the pharmacies in the network?

Question Six: Is a Disadvantage Share Hospital (DSH) eligible for additional benefits by bringing the pharmacy in-house?

Question Seven: What are the pitfalls in using an in-house pharmacy for benefit plans?

Question Eight: What actually happened? Given all this, can a hospital really save money?

Question Nine: What is the best way to start this type of project? How much time is needed?

Question Ten: What are the lessons learned and what can I conclude or expect?

Why should hospitals, pharmacies and pharmacy benefit managers worry about fraud?

The amount of data generated in healthcare is expected to increase significantly in the coming years. There are an estimated 50 petabytes of data in the healthcare realm, which is predicted to grow by a factor of 50 to 25,000 petabytes by 2020 (Knowledgement, 2015). Healthcare payers already store and analyze a significant portion of this data relative to claims. However, to provide the analytic insight, necessary to achieve some of the initiatives noted above, the scope of the payer leveraged information will have to increase significantly to include:

- Provider information: Clinical/medical data (such as electronic health records) are becoming increasingly available to Payers via reciprocal arrangement with Providers.

- Social Data: A growing ocean of data related to patient/member behavior and sentiment is potentially valuable in many analysis scenarios. Social media feeds (Facebook, Twitter, etc.) and consumer information and feeds from sites like PatientsLikeMe.com can be mined to spot trends, monitor opinions, and test hypotheses.

- Government data: Population and public health data from such bodies as the National Institutes of Health (NIH), health.gov, and the Center for Medicare and Medicaid Services (CMS) provide a broad base of medical, epidemiological and demographic information.

- Pharmaceutical and Medical Product Manufactures Data: Research and development data, including clinical trials, is becoming more and more publicly available.

- Information Aggregators: An expanding universe of the third party (for-fee) data collectors and synthesizers is servicing the growing data marketplace for healthcare related data.

With data passing through the many hands of social media, information aggregators and others, data is bound to get into the wrong hands. In the wrong hands, data can be used as currency and used fraudulently. For example, before electronic medical files, each patient’s information within a physician’s office was contained in a paper file, with thousands of paper files stored in cabinets. Even the most elaborate thieves would have to have great planning and resources to steal this information. Now, all patients’ information is stored in electronic data drives and one wrong person with a password can steal thousands of medical identities in a second.

Why is pharmacy fraud so important to control?

When a physician up-codes a claim to gain higher reimbursement, that provider steals money from the government or from a private insurer, but there is no residual product stolen. For example, up-coding a surgery still means that the surgery was completed but there is no commodity that is stolen. When a pharmacist does the same thing, not only does he steal money, but now there is a commodity that can be stolen and diverted to “street crime, namely prescription drugs. Submit a phantom claim for oxycontin, and not only do you have the money from the claim reimbursed by the insurance company, you have the money than can be used to buy more drugs that can then be sold on the black or gray market. Pharmacy fraud is the only fraud in health care that provide a commodity than can be diverted to street crime.

The FBI estimates that pharmacy fraud is 10% of spend. The National Health Care Anti-Fraud association estimates that fraud is 5% of spend. Our parent company, Pharmacy Outcomes Specialists routinely recovers 1% of spend through desk auditing pharmacy fraud.

What should pharmacies do to prevent fraud?

Whether the pharmacy is an independently owned pharmacy, a chain pharmacy, a distribution facility that handles pharmaceutical products or a hospital pharmacy, there are some basic principles that should guide your pharmacy operation:

- Know your staff – Background checks should be mandatory not only pre-employment but on an annual basis. That week that your technician took off may not have been a vacation in Hawaii but a stint courtesy of law enforcement. Random and for cause drug testing should also be mandatory.

- Lock down your valuables – Inventory should be properly managed and accounted for – a single missing pill could be worth thousands of dollars. Employ Crime Prevention Through Environment Design (CPTED) accepted practices like cameras and audio recording devices, bio-metric scanning for entry and exit of the facilities and within the medication dispensing area.

- Check vendors and neighbors – Is the cleaning service used by your facility allowed after-hours access? Can your neighbors access your pharmacy through the plenum above the ceiling? All of these issues should be resolved through an onsite security assessment.

These are but a few of the topics that we cover in an onsite security assessment.

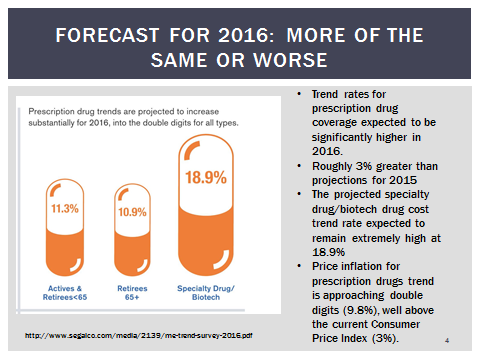

What should those managing prescription drugs expect in cost increases in 2016?

What is so special about COPs?

COPs, or Cluster OPTICS Process uses criminological theory and statistical calculations (deviations from the mean of performance standards) to uncover fraud. This is RADICALLY different from the last 30 years of attempting to detect health care fraud.

In the past, insurance claims processors and adjusters took a “hunt and peck” method to uncover fraud. Basically, every company learned of an issue (i.e. “pill mills”) then went back into the data to see if that situation applied to them. After numerous “queries” into the data, using basic systems like Microsoft Excel or Access, processors and analyst would “discover” fraud. By the time the data was collected, the scheme learned about, the queries run, the fraudsters were long gone with millions of dollars, opening up another pharmacy and starting all over again.

COPs takes a scientific and proactive stance on fraud, particularly pharmacy fraud. Criminological theory tells us two intertwining events take place BEFORE fraudsters commit crime. The Differential Association Theory (DAT) tells us white collar crime is learned…you must be an accountant to learn how to embezzle; you must be a trader to learn securities fraud. With health care, you must have access to the insurance company system and you must know how a legitimate claim looks in order to successfully process a fraudulent claim. Investigators that go to pharmacies, expecting to find that fraudsters who do not have a prescription order and signature logs, are wasting insurance company resources. Insurance fraudsters are “insiders” and know exactly how to manipulate the system because they LEARNED how to exactly commit these crimes through their legitimate business activities.

The second key theory is the Cybercrime Routine Activities Theory (C-RAT). This theory posits that crime occurs when a motivated offender has a suitable target with no capable guardian. Basically, fraudsters prey on victims (patients) who have their identity compromised because those they provide the identity to (physicians and pharmacies) are actually the fraudsters and the insurance company does not have the resources to provide “capable guardianship” over medical identity. In some cases, because insurance companies pass on losses to employers (through group insurance) the insurance company bears no risk and in essence, does not have any interest in providing “capable guardianship.”

Together, learning how to commit crimes through legitimate business transactions and the lack of guardianship provided by the insurance industry leads to C-DAT-RAT theory.

COPs takes claims data as it is produced (online and real time) or within days of being produced and quickly analyzes the dyadic (pair or binary) relationships between pharmacies and physicians, where the criminal behavior is learned and perfected because in order to get away with insurance fraud, physicians and pharmacies need to work together. The intensity of the relationship, combined with the intensity of the amount of claims submitted is analyzed and shown in a Custer Optic graph.

Custer Optics programming is sophisticated analysis that uses SAS programming and once a fraudulent pharmacy is identified, uses that pattern of behavior as the new norm. In essence, as more claims go through the system, and more fraudulent pharmacies are discovered, the system learns from itself and improves its detection abilities. Mean (average) behavior is defined and redefined automatically and deviations from the mean (dyadic pairs that are not “norms”) fall out to the “rim” of normal physician/pharmacy interactions, clustered more in the middle of the graphs.

Once dyadic pairs that are statistically “far” from the mean are discovered, COPs then brings in “big data” from Social media feeds (Facebook, Twitter, etc.) and consumer information and feeds from sites like PatientsLikeMe.com or state license boards (NABP) which can be mined to spot trends, monitor opinions, and test hypotheses.

The COPS product, in summary, identifies inappropriate relationships between pharmacies and physicians, collects social media information about these relationships and provides investigators solid information to start and complete an investigation quickly. This reporting tool can save time and resources in investigating fraud and MORE IMPORTANTLY can find fraud as it is occurring rather than months later when the fraudsters have picked up and moved on, leaving a health plan “holding the bag” of fraudulent payments.

Ten Questions Hospitals Should Ask Before Embarking on an In-House Pharmacy for Employees

Question One: Can the current in-patient pharmacy fit the needs of employees and dependents?

Typically, hospital pharmacies are in the basement or some obscure part of the hospital. In hospitality terms, this is the “back of the house” where real customers do not go. So, for hospitals considering an in-house program, consideration must be given to moving the pharmacy to the “front of the house.” Does the hospital currently have a hospital pharmacy that is tucked away? If so, can approximately 400 square feet within the hospital be devoted to this new endeavour? Recently, one hospital client converted a gift shop which was in an ideal location with plenty of “foot traffic” to the pharmacy. The pharmacy would be most successful if it is also has drive-through capabilities, so being adjacent to an outside wall with a parking lot and plenty of easy access parking is ideal.

While not critical, remember that employees are not the only ones who will need access to the pharmacy, but dependents and retirees need access as well. In the space devoted to the pharmacy, consider a mailing station or a Fed Ex drop box close-by where packages can be mailed to employees, dependents or retirees who do not have daily access to the pharmacy for non-emergency medication. And of course, hospitals are a 24 hour, 365 day operation. If the pharmacy is not open 24 hours, consider a machine that can dispense medication when the pharmacy staff personnel are not available. There are many options available, such as the Asteres Script Center machine. While the outpatient pharmacy personnel are not on duty, counselling can still be made available in off hours by the in-patient pharmacist on duty.

Once the space has been determined and the plans drawn up, a critical step will be to obtain State Board of Pharmacy approval for a retail pharmacy (most states require an additional approval process to convert an “own use” pharmacy to a retail pharmacy). If required, a new NPI number must be secured. Each state differs as to requirements of a new pharmacy, so the Pharmacy Director should check with the local State Board of Pharmacy. It is typical that the State Board of Pharmacy will approve a pharmacy on a temporary basis once the construction and build out is complete, then a final inspection is performed after inventory has been ordered.

Once the pharmacy has been built and initially accredited by the State Board of Pharmacy, inventory must be ordered. The best way to determine what medications to order is to request a report from the current Pharmacy Benefit Manager (PBM). The pharmacy should ensure that any unusual medications that employees may receive are on hand, such as specialty drugs. In order to make the pharmacy most cost effective, the Pharmacy Director should consider making acute care medication available as needed and maintenance medication available either next day or through the mail to employees. Since there is a closed patient group (i.e. the employees and dependents) that are using the pharmacy, the need for long term medication is predictable. Ordering “just in time” medications can help reduce inventory costs. Mailing medications to patients that will need monthly doses of maintenance mediations can also help workflow in the pharmacy as these packages can be prepared and shipped during slow periods in the pharmacy. Calling patients a week or so ahead of the routine monthly fill can help create a better bond with the pharmacy while ensuring the patient still needs the medication, the medication is working properly and the patient is not experiencing any adverse reactions to the medication.

When a hospital uses its own pharmacies for retail, maintenance and specialty prescriptions for employees, it can allow for enhanced savings for the hospital’s benefit program. Promoting the use of hospital pharmacies through plan design encourages employees to use these pharmacies and it can contribute toward additional member cost savings. Further, participants can visit pharmacies close to where they work, making filling and refilling prescriptions more convenient.

Question Two: How can the hospital optimize its wholesaler relationship?

One of the greatest financial benefits that can be most overlooked in bringing pharmacy benefits in-house is that it will greatly increase buying power to the hospital. A rule of thumb is that for every 1,000 employees, $1 million is spent in pharmacy benefits. An average sized hospital employing 2,000 employees can therefore add $2 million in buying power to its wholesaler agreements, if all purchases are directed to the in-patient pharmacy. The following is a checklist when negotiating the wholesaler agreement:

- Increase discounts off brand drugs with higher brand volume

- Decrease the amount of generic drugs that must be purchased through the “house” wholesaler brand

- Increase the amount of funds that must be retained by the wholesaler on account

- Increase the number of days in which the invoice to the wholesaler must be paid

- Increase rebates from the wholesaler

Question Three: How can the hospital pharmacy work with the PBM to get into the PBM’s network and at what reimbursement rate?

Is the hospital pharmacy a profit center or a cost center? If the pharmacy must obtain some level of profit, then the reimbursement rate to the pharmacy must exceed the amount that is charged to the human resource department. If the pharmacy must just break even, then the reimbursement must be exactly the same as the charges to the human resource department. Treat the outpatient pharmacies as a cost center or a profit center, depending on the hospital’s preference or financial objectives.

The Pharmacy Department and the Human Resource Department must work with the Finance Department on the issue of whether or not the pharmacy will create a profit by charging the Human Resource Department more than actual costs of the medication. This single issue can often be the most contentious issue that the project will address.

Once it is determined how much, if any, the pharmacy must make as a profit, start with the cost of the drugs from the wholesaler. Say the wholesaler agreement indicates that brand drugs are purchased at Wholesale Acquisition Cost (WAC) minus 3%. And let’s assume that the pharmacy does not need to make a profit. The PBM agreement must then state that the in-house pharmacy will be reimbursed for brand drugs at WAC minus 3%. However, the PBM agreements with the Human Resource Department are typically stated in terms of discounts off Average Wholesale Price (AWP). For brand drugs, there is a 20% mark-up between WAC and AWP (WAC equals AWP minus 20%). Therefore, the discounts off AWP that the Human Resource Department must negotiate with its PBM should be AWP minus 23%. Having the Human Resource Department and Pharmacy Departments work together with the PBM to ensure that the PBM is not taking spread is an unusual paradigm for the industry and it is critical that the PBM involved be one that is totally transparent and willing to work with the hospital in establishing pass through rates in BOTH the pharmacy reimbursement contract and the HR administration contract.

As a last reminder, some states such as Illinois require tax on prescription drugs. Ensure that any tax or other financial requirements are factored into reimbursement rates.

Question Four: Will bringing the pharmacy cost in-house work with all PBMs?

No. This model can only work when the PBM is totally transparent. Why? Because if a PBM is “taking spread” – that is adding costs to the reimbursement to the pharmacy – then the PBM will no longer be willing to take spread on pharmacy claims for the “star pharmacy” of the PBM’s network. The following is a list of other issues that can impair the use of an in-house pharmacy when working with a traditional PBM relationship (i.e. not a transparent or pass through arrangement):

- Lack of access to information – it is difficult at best to obtain claims information from a PBM that is retaining spread because the hospital organization will be able to see “both sides of the transaction.” The hospital will be able to see what it is being reimbursed and what the Human Resource department is being charged. As a result, PBMs who are taking spread which is not disclosed will not readily be interested in sharing this information.

- Formulary Management – Another option for hospitals is to work with its PBM to develop a managed formulary for employees. All hospitals already have a managed formulary in place for hospital inpatients. If the hospital pharmacy fills prescriptions for employees (in addition to inpatients), it increases the volume of use for that formulary, which helps when purchasing from a wholesaler.

Question Five: Should plan design differ between the in-house pharmacies and the rest of the pharmacies in the network?

The hospital as an enterprise should set objectives for use of the in-house pharmacy. Should patients be encouraged to use the in-house pharmacy through copays? At what level should the copays be set? Should all limits (such as quantity limits) and Prior Authorization requirements be eliminated from mediation obtained through the in-house pharmacy? Offering a plan design that provides lower copays for employees when they frequent outpatient pharmacies versus other network pharmacies will quickly and effectively encourage the use of the in-house pharmacy.

Different hospitals have reacted differently to the issues of plan design. One hospital that was a client did not allow employees in a four county region that is serviced by the hospital to go “out of network” or use the PBM’s national pharmacy network (of course, employees can use out of network pharmacies but it is not covered under the benefit plan). The national PBM network is only permitted under the plan if the employee, dependent or retiree obtains the medication outside the four-county area. Other hospitals merely encourage the use through lower copays. If the hospital has a large, front end deductible and a Health Spending Account (HSA), be careful that the plan design keeps within the limits for HSA accounts. The front end deductible cannot be waived for just the in-house hospital pharmacy.

Hospital employee plan design and formulary innovation is a leading reason to promote the in-house pharmacy. Options that support monetary savings for the hospital or its employees include:

- Percentage copays, or coinsurance. Using percentage copays instead of flat dollar copays hedges against the inflationary cost increases year over year. These features also help educate members about the true cost of their medications.

- $1 generic copay medication list for employees. Developing a select list of generic medications that are available for $1 a month and $3 for three months is an excellent cost-savings approach. These copays would be available only at the hospital’s pharmacies for its employees and their dependents. Hospital employees are thus encouraged to utilize hospital-owned pharmacies and to use generic drugs. Hospital employees are typically the most educated and knowledgeable about the advantages of generic drugs.

- Another option for hospitals is to work with their PBM to develop a managed formulary for their employees. All hospitals already have a managed formulary in place for hospital inpatients. If the hospital pharmacy fills scripts for employees (in addition to inpatients), it increases the volume of use for that formulary, which helps when purchasing from a wholesaler.

One area of considerable cost savings is to utilize a hospital’s in-house pharmacy to fill maintenance and specialty prescriptions. The hospital may want to mandate that maintenance and specialty prescriptions can only be filled by the in-house pharmacy to maximize cost savings. Since these medications can be predictable, patients can request that these medications be mailed or messengered to the patient’s home, regardless of where the patient lives.

If the hospital has no employees outside of the area serviced by the hospital (such as no retirees), one might argue that no additional network is needed. However, keep in mind that some employees might not want the hospital/employer to be aware of certain medications that are needed for patients and may prefer the anonymity that comes from purchasing medication outside the system but still under a benefit plan.

Question Six: Is a Disadvantage Share Hospital (DSH) eligible for additional benefits by bringing the pharmacy in-house?

Becoming a contracted pharmacy to distribute 340B or GPO prescriptions for qualified entities can lead to significant cost savings for purchasing brand drugs by the DSH hospital. Savings can exceed 80% discounts off AWP for brand drugs using 340(b) pricing. Taking advantage of additional savings that are available through a 340B or GPO “own use” program for its employees by accessing these deeper discounts will result in reduced costs. But this project requires additional steps and assistance such as the following:

- Retain an attorney who is an expert in 340(b) requirements to ensure that the hospital and the employed physicians have met all of the 340(b) requirements.

- In addition to requirements for employed physicians, patients must meet additional requirements such as being seen by the employed physician at the DSH hospital and the medication must be prescribed at that location.

- A closed network of pharmacies must be implemented to qualify for 340(b) pricing and the inventory within those pharmacies must be replenished using only bottles of 340(b) priced drugs. In other words, inventory must be separated and only replenished with new 340(b) purchased medication.

There are firms that specialize in assisting hospitals with both 340(b) “front-end” eligibility requirements for the hospital, physicians and patients and in the “back-end” replenishment. Certainly, using these firms and their expertise is critical in ensuring that all requirements are met.

Question Seven: What are the pitfalls in using an in-house pharmacy for benefit plans?

There are unique opportunities for hospitals in using in-house pharmacies. However, there are also certain pitfalls of which hospitals should be aware.

A. Lack of access to information. Many hospitals (and employers in general) have difficulty verifying what is being received from their relationship with their PBM. Often the PBM is not performing at the discounted levels indicated in the contract. Many PBMs do not allow clients to independently verify or audit what it happening with their prescription drug claims. The PBM could easily be retaining client dollars through spread, data sales or other undisclosed arrangements with pharmaceutical manufacturers.

B. Zero administrative fee/transparency/pass through pricing and formulary games. PBMs that do not charge an administrative fee to provide services are really charging through undisclosed spread taken in claims processing or retention of rebate payments from drug manufacturers. When was the last time a company provided services entirely for free? How long would such a company survive? While these questions also apply to PBMs, the enticement of zero administrative fees through the RFP process tempts organizations purchasing PBM services. Now, when a hospital client wants a transparent arrangement on a majority of claims that will be processed through the in-house pharmacy, the PBM wants to charge a ridiculously high administration fee that may wipe out all savings resultant from the in-house pharmacy. This situation, once exposed, may in turn lead the hospital to finding a PBM that will work in an economical manner (such as privately held PBMs) with full transparency. But, this leads to “two steps forward, one back.” An additional project of finding and implementing a new PBM may derail the in-house pharmacy for months.

A PBM should be an advocate for its clients. But in many cases, PBMs profit off certain aspects of their client’s programs. For example, a PBM might not desire to promote hospital outpatient pharmacies because it may prefer to promote its own network pharmacies, where it can obtain spread on the claims dispensed. When a PBM won’t allow such flexibility, it should be a red flag to a hospital seeking a PBM that works solely as an advocate for its clients.

Use this checklist when selecting a hospital PBM:

- Ensure your PBM is employing a total pass-through business model PBM for retail network claims, specialty claims and mail order and is indifferent to the using the retail network, mail order or specialty program offered/owned by the PBM or the hospital

- The PBM employees a lowest-net-cost, managed formulary for hospital employees and dependents

- The PBM should support the hospital’s decision to use the hospital outpatient pharmacies as a cost/profit center and subsequently the use for retail, maintenance and specialty distribution options and should be willing to implement the pricing structure of the hospital rather than its own pricing structure.

- The PBM supports utilizing innovative plan designs, such as $1 generic programs at the hospital’s outpatient pharmacies.

- The PBM assists or does not hinder conducting clinical programs that promote cost savings through aligned incentives between the PBM and the hospital.

- Unwillingness of wholesaler to re-align pricing points, contract terms with additional volume. With the additional volume, the wholesaler should work with the hospital to improve the purchasing of prescription drugs. If the current wholesaler is not willing to work with the hospital, the hospital should consider moving to a Group Purchasing Organization (GPO) that might have additional advantages. While there are only three national wholesalers in the United States, these wholesalers fight very aggressively for business and, just like with the PBMs, it may take a move in wholesalers to gain advantages with the additional volume. However, unlike with the PBM move, the wholesaler move is often much more difficult because many of the systems that are needed to operate a pharmacy are tied to the wholesaler relationship.

- The hospital itself. One of the most derailing aspects of these projects is the hospital itself. Once exposed that there are profits to be had within the pharmacy, there is no consensus as to how much profit is reasonable for the pharmacy to take. Once discovered that the pharmacy benefit has not been properly managed through a transparent contract, the human resource department is unwilling to change PBMs or its contract terms. How much should be subsidized in lower copays to encourage members to use its pharmacy? The more silos a hospital has, the worse the in-hospital battles. These battles are exacerbated, unlike in other industries, by “medical professionals” who may have an over inflated opinion of their own ability to manage prescription drug costs. Sounds like your hospital? If so, take a deep breath. Remember the goal of the in-house pharmacy: to lower cost through a convenient distribution channel to employees and dependents.

Question Eight: What actually happened? Given all this, can a hospital really save money?

Yes. Taking a 3,500 employee hospital, the below chart illustrates savings to both employees and the hospital.

| 2012 Original | 10% In-house | 20% In-house | 30% In-house | 40% In-house | 50% In-house | ||||||

| Total Cost | $4,700,361 | $4,650,421 | ($49,940) | $4,600,484 | ($99,877) | $4,550,482 | ($149,878) | $4,500,511 | ($199,850) | $4,450,511 | ($249,850) |

| Mbr Cost | $1,107,887 | $977,257 | ($130,630) | $922,870 | ($185,017) | $868,331 | ($239,557) | $813,944 | ($293,943) | $759,391 | ($348,496) |

| Net Cost | $3,592,474 | $3,673,163 | $80,690 | $3,677,613 | $85,140 | $3,682,152 | $89,678 | $3,686,567 | $94,094 | $3,691,119 | $98,646 |

This hospital spends approximately $4.7 million in prescription drugs in 2012, $1.1 million borne by members and $3.6 million borne by the hospital. Depending on the amount of prescription utilization that will “go in-house” (we modeled from 10% in-house to 50% in-house in year one), reduced costs vary from $4.6 million (at 10% in-house) to $4.4 million (given 50% of in-house use). So overall the hospital and its members will save about $300,000 (not taking into consideration inflation of drug costs) or about 5% of costs. But in addition to reducing overall costs, members will save about $350,000 mainly through reduced copays to use the in-house pharmacy over the PBM’s retail network and mail order facility, while the hospital will spend about $98,000. The increased cost to the hospital was agreed upon by the hospital to encourage the use of the in-house hospital because using the in-house hospital created additional advantages for the hospital that the hospital believes will be more than offset in years to come such as improved wholesaler terms, increased use of generics, increased purchase and better management of specialty drugs. Of course this hospital decided to decrease copays drastically in order to encourage use of the in-hospital pharmacy. If copays had not been lowered so drastically, the hospital could have recouped all of the savings resultant of lower costs.

Question Nine: What is the best way to start this type of project? How much time is needed?

Without a doubt, a multi-disciplinary team both internally and externally is needed. At a minimum, the internal team should consist of representatives from the pharmacy department, the human resources and the finance department. Externally, the hospital should have a pharmacy consulting team that is expert with wholesaler agreements and PBM agreements for benefit management and for pharmacy contracting along with a pharmacist that is familiar with your state(s) regulations and Pharmacy Board. If 340(b) pricing is involved, an attorney will be necessary for 340(b) pricing compliance issues which are numerous. The PBM and wholesaler should also be involved in the process and it should be determined very early in the process if these outsider vendors are “good to go” with the project or will provide additional impediments.

These projects can be completed in as little as six months, including the build out of a pharmacy within the hospital. If a new PBM or wholesaler agreement is needed, allow an additional six months, or a year in total.

Question Ten: What are the lessons learned and what can I conclude or expect?

If every aspect of the project goes smoothly, expect lower costs for prescription drugs, happier employees who do not need to drive to a pharmacy when one is available at work and a better managed prescription drug program through tighter contracts with the PBM and wholesaler and “hands-on” management performed by dedicated pharmacy employees. But through the lessons learned on your project, you might also learn that PBM relationships are complicated at both ends – both in contracting for reimbursement and contracting as an employer. You may also learn that you have options for your wholesaler agreement or that your agreement can be substantially improved which you never believed possible. You might also learn that the pharmacy can be a cost and profit center. You might learn that there are many options to managing the prescription drug program through tighter networks (including the “anchor” in-house pharmacy), aligning the in-patient and in-house formularies, imposing or dropping limits on specialty and other high cost or abused drugs and empowering the pharmacy to counsel patients on drug use and misuse. In summary, you may learn that your hospital has a better managed pharmacy program – which may be expected – combined with many unexpected lessons on project management within a complicated hospital system.